What Is Banking-as-a-Service (BaaS) and Why Does It Matter?

Banking Infrastructure, Unbundled

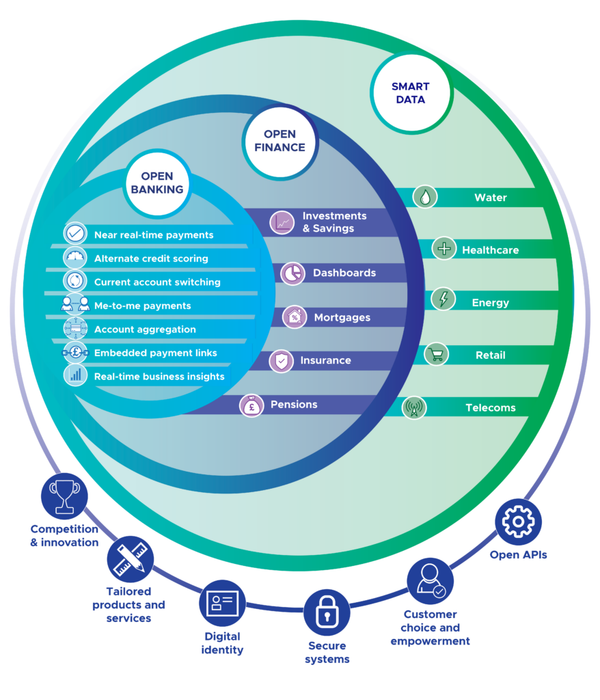

Banking-as-a-Service (BaaS) is a model where licensed banks provide their core infrastructure — account management, payments processing, compliance, and regulatory licensing — to non-bank companies via APIs. The non-bank uses this to offer banking products under their own brand.

A Concrete Example

A payroll software company wants to offer instant wage advances. Rather than spending years obtaining a banking licence, they connect to a BaaS provider like ClearBank or Griffin. The BaaS provider handles the licensed banking layer; the payroll company builds the user experience. The end customer sees a seamless branded product with banking infrastructure running invisibly underneath.

Key UK BaaS Providers

- ClearBank: UK's first new clearing bank in 250 years; provides real-time clearing to fintechs

- Modulr: Payments-as-a-Service used by Sage and others

- Griffin: Full-stack BaaS with its own UK banking licence

- Railsr: Global BaaS platform with FCA authorisation

Why It Matters for Consumers

BaaS enables embedded finance — buy-now-pay-later at checkout, instant insurance alongside holiday bookings, or business accounts built into accounting software. Financial services appear exactly where and when needed, without redirecting to a separate banking interface.

Regulatory Implications

The FCA's Consumer Duty rules place obligations on all firms in the distribution chain — meaning BaaS providers and the brands using their infrastructure both carry responsibility when things go wrong. This is actively shaping how the market evolves.