The Future of UK Banking in 2026 and Beyond

Where UK Banking Stands in 2026

UK banking in 2026 is a sector in active transition. Digital-first challengers have moved from novelty to mainstream — Monzo alone serves over ten million customers, Starling is profitable, and Revolut is valued among Europe's most valuable private companies. Traditional banks have responded with significant technology investment and product improvement.

The Key Trends Shaping What Comes Next

AI Integration Deepens

Artificial intelligence has moved from fraud detection (where it's mature) to personalised financial advice, automated savings optimisation, and proactive financial health monitoring. Banks are experimenting with AI-driven overdraft prevention, spending coaching, and automated tax preparation. Regulatory guidance on AI in financial services is still developing, creating both opportunity and uncertainty.

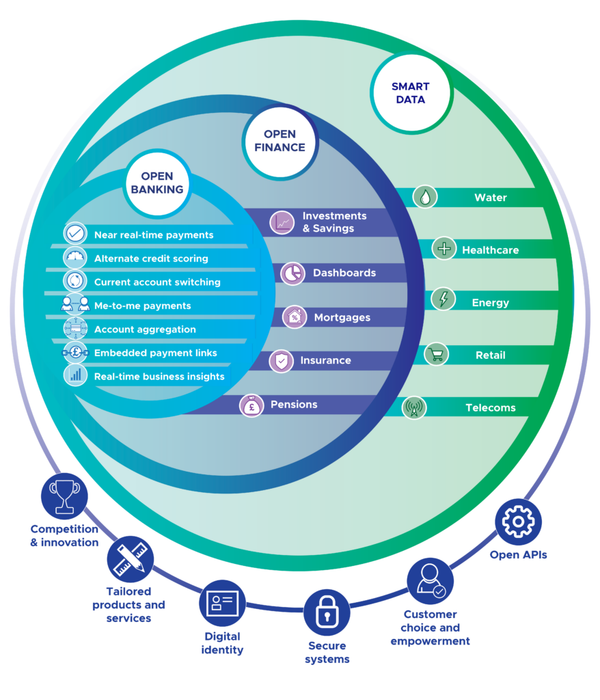

Open Finance Rolls Out

Open Banking's extension to pensions, investments, mortgages, and insurance — Open Finance — is progressing through UK legislation. When implemented, it will enable consumers to see their complete financial picture across all providers and switch or optimise products with dramatically less friction.

Payments Infrastructure Modernisation

The UK's New Payments Architecture (NPA) will replace the existing Faster Payments infrastructure over the coming years, enabling richer payment data, account-to-account payments competing directly with card networks, and better real-time fraud prevention.

Branch Networks Continue to Shrink

Traditional banks continue rationalising physical networks, replaced by banking hubs shared between multiple banks and enhanced Post Office services. The regulatory debate about cash access continues, with legislation requiring banks to maintain minimum cash access standards in communities they serve.

The Consumer Opportunity

British consumers have never had more choice, better tools, or stronger regulatory protection in banking. The convergence of competition, technology, and regulatory pressure continues to push standards upward. The informed consumer — who switches for better rates, uses digital tools for budgeting, and understands their rights — is the one who benefits most from this transformation.